Moving from a pension-driven retirement to a 401k-driven retirement has not been easy. Because the employee not only has the responsibility for saving but also to make sure the assets grow enough to meet an income-funding goal, they are responsible for ongoing investment management too.

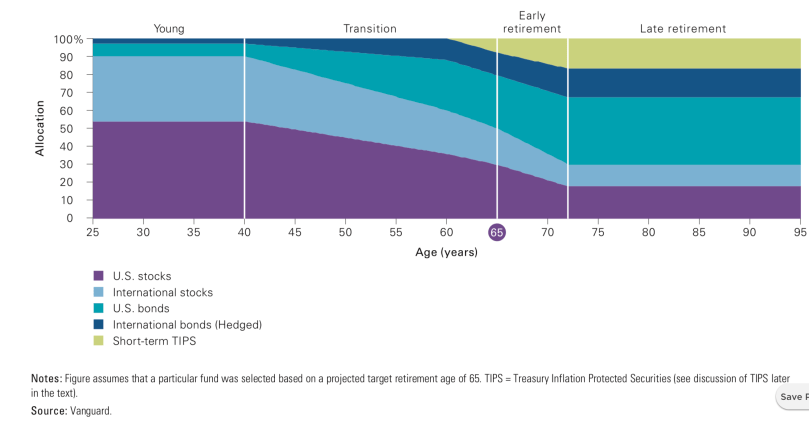

Efforts from employers, plan providers, and investment management companies have helped. One major innovation was the target-date fund. Target-date funds are an all-in-one investment solution. The risk tolerance and diversified investment mix is based on your age and the number of years until retirement. As the employee moves forward through time, the risk is gradually reduced. This reduction in risk is called a glide path. Glide paths will vary with each investment company.

On the surface,this seems perfect for employees! The automatic risk reduction would save them from themselves. 2009 is a perfect example. Many employees nearing retirement enjoyed the booming stock market but never considered that the risk party could end. When housing prices plunged along with their 401k and sometimes the loss of a job, many wished they had been on a glide path that helped protect their income-replacement nest egg.

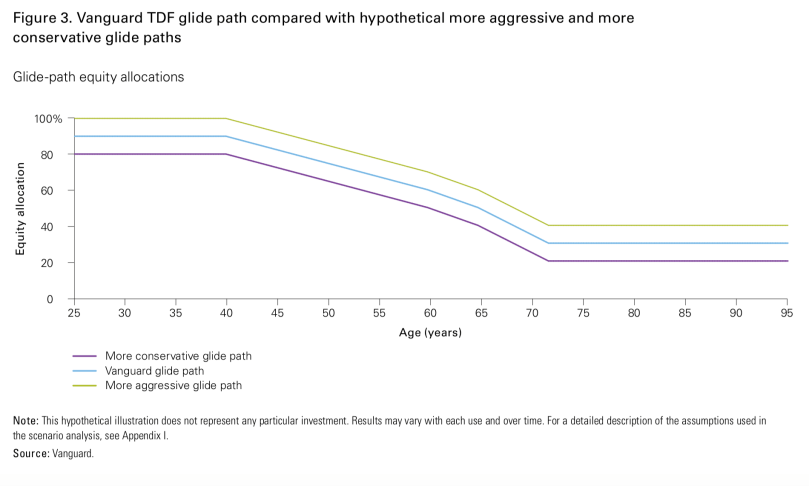

So what could be the downside? The problem is the target-date fund does not alleviate the employee of all risks. Take Vanguard as an example, even well into retirement; the retiree still has 30% exposure to equities. It is not that the 30% may not be appropriate, with our longer time in retirement and our need to keep up with inflation, especially healthcare inflation, it may be needed. The problem is the employee still doesn’t understand the risk they are taking on. I have had many employees think that once they got to their target date, there was no risk in the portfolio. Not only do they still have market risk, 50% at age 65 for Vanguard’s glide path, but they also have some interest rate risk with the bond funds they hold. Imagine if we had an extended period where rates were rising unexpectedly, and the stock market declined at the same time. It is not inconceivable that both the employee’s bond and stock funds could go down at the same time.

The unexpected usually gives us fewer financial options and the shocking more emotional obstacles. The problem with retirement is that we are at our most financially vulnerable. So when a retiree thinks that that target date is a magical “everything-is-fine” date, there could be trouble.

All the auto enrollment of target-date funds in the world will not negate the fact that employees are responsible for their own retirement and must know what they are invested in and why. They must have at least some idea of the return needed to reach goals and the risk that must be taken on to get said return.

Pensions are not coming back. 401ks are a great way to save for what Social Security and Medicare don’t cover, but it takes some degree of knowledge and management to be a good steward of the 401k. Attempting to do everything for the employee while teaching them nothing, is a recipe for disaster. The employee will suffer from this approach.

Stay financially classy Minnesota!