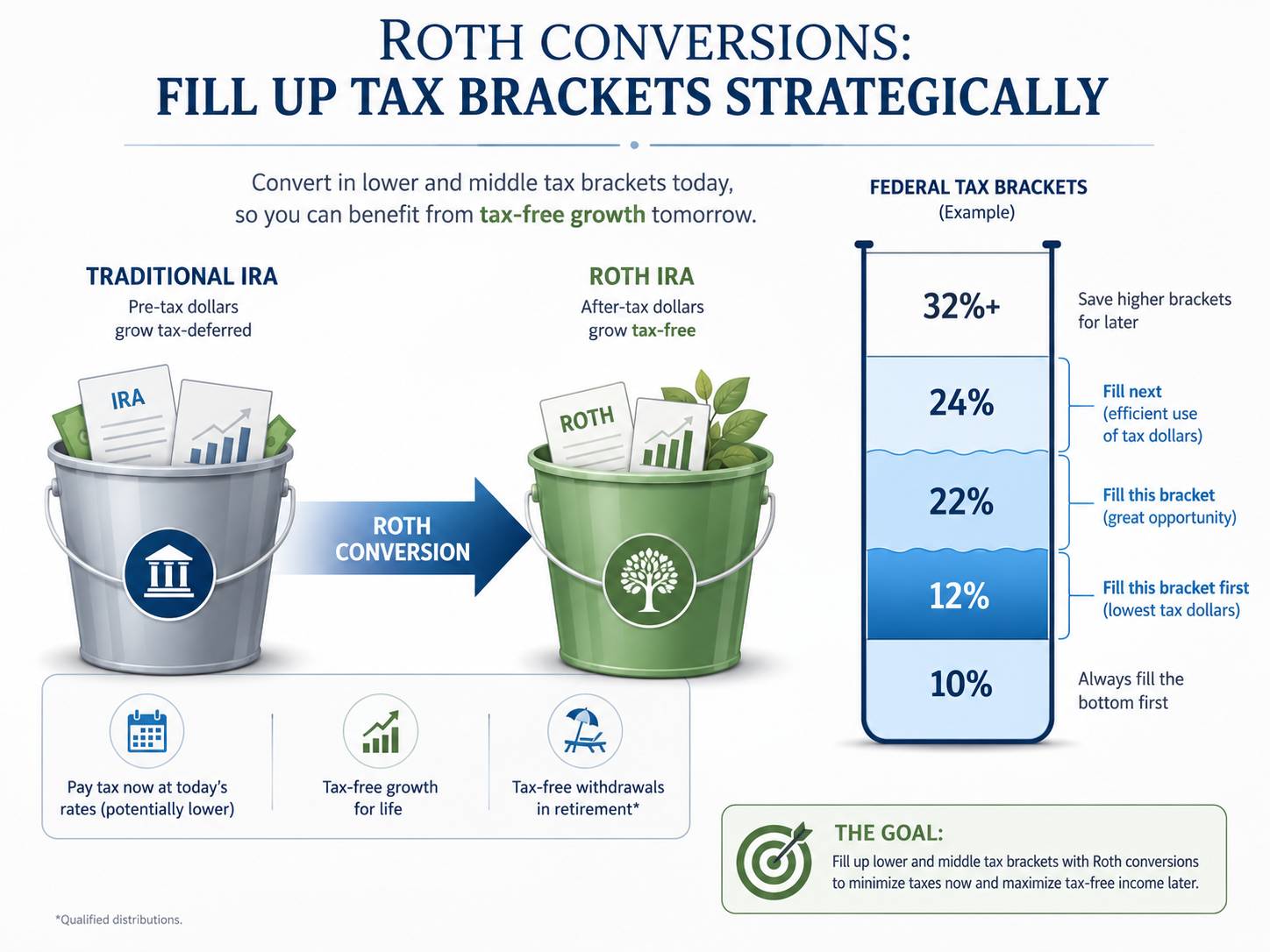

Roth conversions can be one of the most effective retirement tax-planning strategies available. Done properly, they may help reduce future Required Minimum Distributions (RMDs), create tax-free retirement income, and improve flexibility later in retirement. But Roth conversions are not automatically beneficial. Poorly timed or oversized conversions can actually increase lifetime taxes. Here are five of the most common Roth conversion mistakes retirees and pre-retirees make. 1) Waiting Too Long to Start Roth ConversionsMany people wait until RMDs begin before considering Roth conversions. By then, taxable income is often already elevated from: Social Security Pensions Investment income Mandatory IRA withdrawals For many retirees, the best Roth conversion window occurs: After retirement Before Social Security Before RMDs begin These lower-income years may allow retirees to convert money at lower tax rates before future income rises. 2) Converting Too Much in One YearLarge Roth conversions can unintentionally: Push retirees into higher tax brackets Trigger Medicare IRMAA surcharges Increase Social Security taxation Create higher state income taxes Instead of converting everything at once, many retirees benefit from a gradual multi-year approach designed around tax bracket management. A better question is often: “How much can we convert before the next tax threshold is triggered?” 3) Focusing Only on This Year’s TaxesMany investors avoid Roth conversions because they dislike paying taxes today. However, retirement tax planning should focus on lifetime taxes, not just this year’s bill. Strategic Roth conversions may help reduce: Future RMDs Survivor tax issues Taxable income later in retirement Taxes paid by heirs Paying taxes at a known rate today may be preferable to facing larger required withdrawals and potentially higher tax rates later. 4) Ignoring Medicare IRMAA SurchargesOne of the most overlooked Roth conversion mistakes involves Medicare premiums. Large Roth conversions can increase modified adjusted gross income (MAGI) enough to trigger IRMAA surcharges for Medicare Part B and Part D. Even small increases above an IRMAA threshold can lead to meaningful premium increases. Good Roth conversion planning should coordinate: Tax brackets Medicare premiums State taxes Long-term RMD projections 5. Converting the Wrong Assets 5) Not all Roth conversion dollars are equally valuable.Many retirees convert: Cash Bonds Lower-growth investments while leaving higher-growth assets inside traditional IRAs. Because future Roth growth may become tax free, higher-growth investments may benefit more from being inside the Roth account over time. Market downturns can also create attractive Roth conversion opportunities if assets later recover inside the Roth IRA. Final ThoughtsRoth conversions can be a powerful tool for reducing lifetime taxes, but successful strategies are usually: Gradual Tax-aware Flexible Revisited regularly The goal is not simply converting money to a Roth IRA. The goal is creating a more tax-efficient retirement income plan over the long term.

Mark Struthers, CFA, CFP®, CEPA, RMA® For current clients looking for a meeting:

This commentary is provided for general information purposes only, should not be construed as investment, tax, or legal advice, and does not constitute an attorney/client relationship. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable, but is not guaranteed. |

Top 5 Roth Conversion Mistakes That Can Increase Lifetime Taxes

Categories

- 401k

- Backdoor Roth

- Bitcoin

- College Funding

- Crypto

- Economics

- Estate Planning

- Featured

- Feel Good

- Financial Planning

- Healthcare

- healthcare

- HSA

- Inflation

- Insurance

- Investing

- IRA

- Mega Backdoor Roth

- Open Enrollment

- Podcast

- Private Equity

- Retire Early

- Retirement

- Roth IRA

- SEPP

- Social Security

- Student Loans

- Taxes

- Traditional IRA

- Uncategorized

Share this post:

If you don’t have a plan and would like to get one, schedule a Discovery Meeting:

Mark Struthers, CFA, CFP®, RMA®

For current clients looking for a meeting:

This commentary is provided for general information purposes only, should not be construed as investment, tax, or legal advice, and does not constitute an attorney/client relationship. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable, but is not guaranteed.