The Oedipus Effect

The Oedipus Effect refers to the phenomenon where a prediction or belief about an event influences behaviors in a way that causes the prediction to come true. The term is inspired by the story of Oedipus in Greek mythology, where attempts to avoid a prophecy inadvertently lead to its fulfillment.

“What walks on four feet in the morning, two in the afternoon, and three at night?”

The answer is man. But what may be more of a riddle is why what makes America so strong also makes it weaker.

Why is the American economy so powerful? There could be many answers: less regulation, more innovative tech companies, liquid and transparent capital markets—I’m sure I missed some. One may be that we are a consumer-driven economy, 70% consumer-driven, so we are not dependent on demand from other countries. The downside to this is that our buying is based on mood. It does not make any difference if our job is good and our standard of living is high; we can talk ourselves into a recession, even if one could have been avoided.

Without getting into the story, the Oedipus Effect is often discussed in sociology and philosophy, particularly in the context of self-fulfilling prophecies. For example, if people believe a bank is failing and rush to withdraw their money, their actions can cause the bank to collapse, fulfilling the original belief. Sphinx riddling, father killing, and mother marrying aside, if fear of tariffs and inflation causes spending to pull back, the recession will come. This is not meant to scare you, but knowing possible outcomes helps us make better decisions.

On the positive side, if the tariffs go away and the mood changes in time, the recession could be avoided. If you start to “plan” for the recession, make sure it is tactical and part of your overall strategic plan.

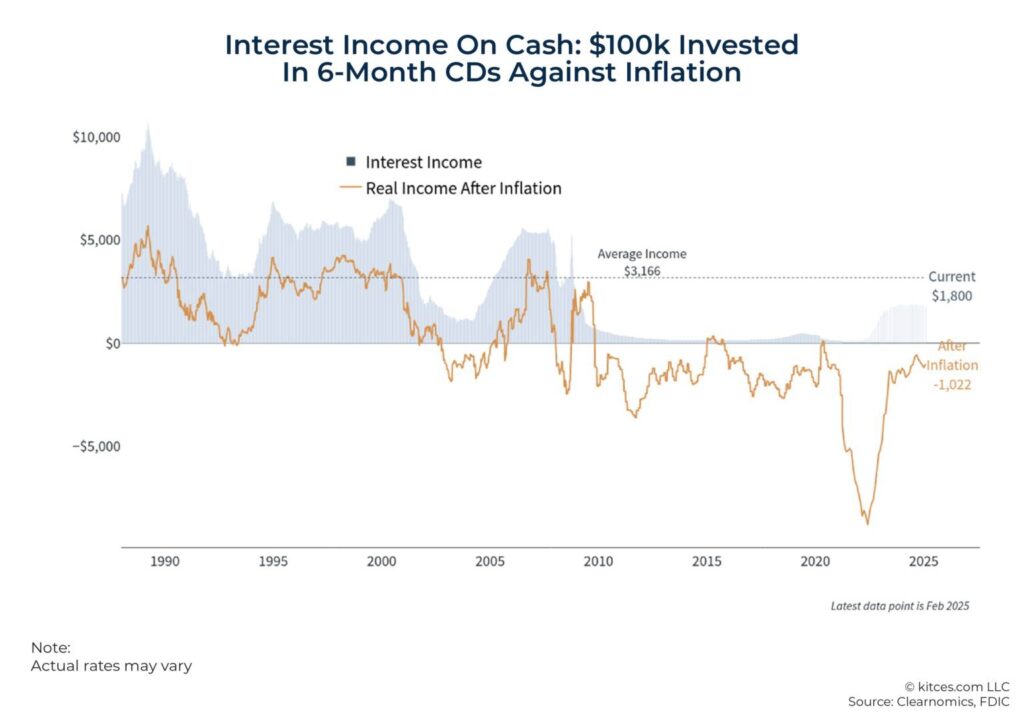

Recessions Are Not Always a Heart Attack & Cash Is Not Always Comforting

One issue Americans have is that they tend to think that recessions are always closer to heart attacks than a cold. It’s probably because our recent recessions were very dark and scary, 2009 and COVID. While COVID was short-lived, it was pretty dark and scary in the Spring and Summer of 2020, and the Great Recession was closer to a depression than a recession. Unemployment reached 14.7% for COVID and over 10% in 2009, much higher for some industries. And some would argue that both were more artificial recessions.

Any recession is not fun if you are the one getting laid off, but mild recessions can last 8-9 months, and the unemployment rate can stay under 6%-7%—these can easily be weathered with just a little planning. They are over quickly. While beefing up your emergency fund is not a bad idea when the chances of a recession increase, if you go too far, you may sacrifice more than you think.

It’s understandable that, in this volatile environment, investors are retreating to the perceived safety of cash. Unlike stocks or bonds, cash holdings appear stable, offering a sense of security. However, this safety is often an illusion when viewed through a long-term financial lens — M. Kitces

There is nothing wrong with “comfort cash,” but any action should be tactical within your overall strategic plan.

A good article from Mark & CNN on comfort cash: https://www.cnn.com/2022/07/20/success/401k-investors-bear-market/index.html

Don’t sacrifice short-term comfort for long-term pain, especially when we could have a “normal” recession. Planning is about dealing with possible uncertain outcomes with limited resources and time. We never know when the next big recession will happen; all we can do is plan as best we can for all scenarios, given your age, but we can never time a recession. On a recent call, a client quoted me to me…….

Even if you time the get-out, when do you get back in? — Sona Client

If you spend all your time hiding in the basement bracing for Armageddon, you risk sacrificing the very thing you aim to safeguard.

Click below for your free emergency fund guide:

What-Issues-Should-I-Consider-When-Establishing-And-Maintaining-My-Emergency-Fund-2025.pdf

What Can I, As A Consumer, Do About Tariff Inflation?

The most important thing consumers can do now to combat higher prices is to follow the two S’s: saving and substitution, says certified financial planner Mark Struthers at Sona Wealth Advisors in MarketWatch.

“Avocados mostly come from Mexico. What could you substitute them with? Part of the substitution might be to delay a purchase, like a vehicle. Vehicles will take a big tariff hit, too. Spruce up your old vehicle to last a few more years. Unfortunately, most of the lumber comes from Canada, so if you’re not a homeowner yet, you may have to start planning to rent for a bit longer. Planning can make the best of the situation,” says Struthers.

Read the full article, including advice from other advisors, here: https://www.marketwatch.com/picks/this-is-exactly-how-much-trumps-tariffs-might-cost-you-new-report-finds-we-hear-theres-a-2-pronged-way-for-consumers-to-deal-fe17560c?mod=home_ln

The New Paradigm

Retirement is about redistributing time, not just extending it — Simon Chan

I only use fancy words if I have to. But paradigm (pair of dimes) seems appropriate here. Retirement used to be to retire around age 65 and then spend 10-15 years in retirement. Planning for 12-18 years with a pension was not too difficult. Inflation is rarely much of an issue. Now we are retiring around the same time or a little earlier, but we are planning for 25-30 years. With this new paradigm, folks are spending as much time in retirement as they did working. But our approach to retirement has not changed.

One thought from a recent Simon Chan article was that instead of a 35-40-year work sprint, we should pace ourselves for a 50-60-year more enjoyable marathon. Most people I know over age 65 easily have time to work part-time; some even do; they go back to work. What if it was planned? Would they have more options? Would there be a more robust financial, emotional, physical, and social life?

The old model treated retirement as a finish line — Simon Chan

I recently spoke to two clients who had successfully planned second acts. Well-planned second acts. In each case, one spouse started a “dream” career, which they did not mind working until at least age 65-70. In each case, the other spouse was planning on leaving high-stress jobs for part-time work or was at least willing to do so. (And I believe them both — some folks say that to make the number look good.) In each case, the couples were surprised by what this extra enjoyable (or at least semi-enjoyable) work did to their plan. They had more options. In this case, the options had to do with risk. They had a wider range of acceptable risk levels to reach their goals. There is flexibility and comfort in having options. What I find interesting is that it is clear that many Gen Xers will be as healthy at 65 as previous generations were at 50.

If 65 is the new 55, shouldn’t we plan like it is?

The rocking chair is no longer for the 60s and 70s, but for the 80s or 90s. We are more active than ever. There are as many 60-somethings as 30-somethings in my competitive Saturday pickleball group. For fun, below are some photos of the World’s Best cinnamon rolls I brought for the group. A client gave them to me. Thank you! You know who you are. They loved them! I’m not sure if they are worth an hour of waiting, but many thought they were!

Check out my conversation with Alara, a non-financial retirement coach. She helps with the new “pair of dimes.”