|

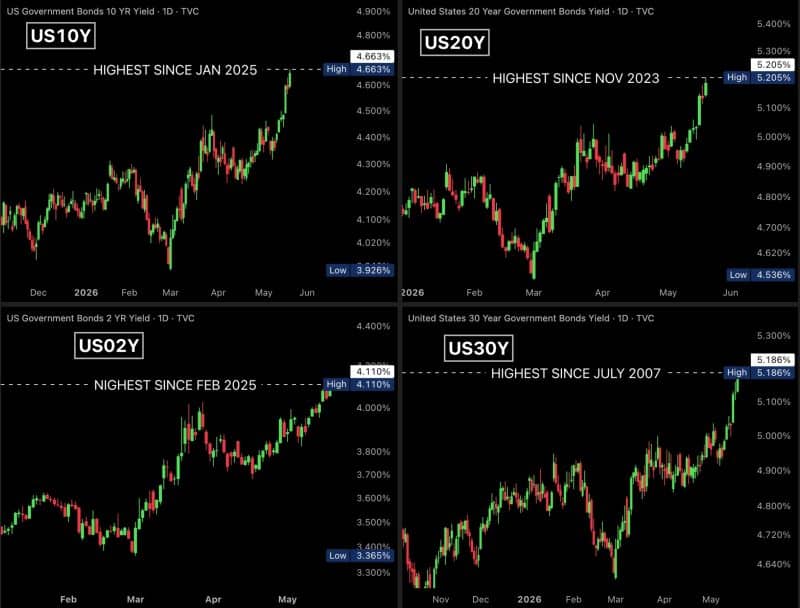

Over the last few years, many investors learned a painful lesson: Bonds are not always “safe” in the way people assume. Many people learned that in 2022. Now, with long-term Treasury yields climbing back toward levels we have not seen since before the Global Financial Crisis, investors are once again asking: • Is the bond market breaking? • Are higher rates bad for stocks? • Should retirees still own bonds? • And what happens next? The reality is more nuanced than the headlines. Why Bond Yields Are RisingRecently, Treasury yields surged higher: • 10-Year Treasury near 4.7% • 20-Year Treasury above 5.2% • 30-Year Treasury above 5.1%

Financial media often frames this as a “bond market meltdown.” But rising yields are not automatically a crisis. Bond yields generally rise for four main reasons: Persistent Inflation ConcernsEven though inflation has cooled from peak levels, markets are not convinced inflation is fully defeated. Investors demand higher yields when they fear future purchasing power erosion.

Massive Government BorrowingThe U.S. government continues issuing enormous amounts of debt. More bond supply generally requires higher yields to attract buyers. This is partly a math problem. Higher-for-Longer Interest RatesFor years, investors assumed rates would quickly return to near zero. Now markets increasingly believe: • structurally higher inflation • stronger nominal growth • large deficits could keep rates elevated for much longer. Investors Finally Have AlternativesFor over a decade, “TINA” dominated markets: There Is No Alternative to stocks. Now investors can earn: • 4–5% in Treasuries • attractive money market yields • higher-quality bond income That changes asset allocation decisions. Does This Mean Bonds Are Bad?Not necessarily. In fact, today’s bond market may be healthier for long-term investors than the ultra-low-rate environment we lived through for years. The problem in 2020–2021 was not that bonds existed. The problem was: • investors owned long-duration bonds (very few adjusted for the risk or withdrawal needs) • with historically low yields • and massive interest-rate sensitivity When rates rose sharply, bond prices fell hard. That was duration risk finally mattering again. Very few investors truly understand duration risk and credit risk. Many people view bonds like CDs or fixed annuities — stable, predictable, and insulated from market volatility. But bonds can behave very differently depending on maturity, credit quality, and interest-rate sensitivity. That distinction becomes critically important during retirement distribution planning and Roth conversion strategies. If investors are forced to sell longer-duration bonds during rising-rate environments, losses become real. Proper bond structure, liquidity management, and withdrawal sequencing matter far more than many investors realize – and few people associate bonds with sequence-of-return risk. The Most Important Bond Concept Investors MissMany investors still think: “Bonds are safe because they don’t fluctuate much.” They are often the “blue” part of your 401k statement – soothing – comforting. But bond risk is heavily tied to duration (when they mature). Longer-duration bonds: • are more sensitive to rate increases • can experience large price declines • and behave very differently from short-term bonds A 1–2 year Treasury behaves nothing like a 20–30 year Treasury. That distinction matters enormously in retirement planning. Why This Matters for Retirees Retirement income planning is no longer just: “Buy bonds for safety.” Today, retirees need to think about: • cash flow timing • withdrawal sequencing • inflation • duration management • tax efficiency For example: If a retiree owns long bonds and must sell during a rising-rate environment, losses become real. But if the bond structure is aligned properly with spending needs, volatility may matter far less. This is where bond management becomes more important than simple bond ownership. The Outlook for StocksHigher rates absolutely matter for stocks. When Treasury yields rise: • borrowing becomes more expensive • corporate profits can face pressure • consumers may slow spending • stock valuations often compress That is especially true for: • speculative growth companies • highly leveraged businesses • stocks priced for perfection But rising yields do not automatically mean a stock market crash. Historically, stocks can still perform reasonably well when: • economic growth remains positive • earnings continue growing • inflation stays controlled The bigger issue is that investors may need to adjust expectations. The Era of “Easy Money” May Be OverFor much of the 2010s: • near-zero interest rates • massive liquidity • Federal Reserve support helped push almost all asset prices higher simultaneously. That environment may not repeat. Going forward, markets may reward: • profitability • cash flow • balance sheet strength • valuation discipline far more than speculative growth stories. What Investors Should Focus On Instead of HeadlinesHeadlines like: “The Bond Market Is Melting Down” generate clicks. But long-term investors should focus on: • portfolio structure • risk management • diversification • tax planning • spending flexibility In retirement planning especially, success is often less about predicting rates and more about building a strategy that can adapt to multiple market environments. That includes: • thoughtful bond duration • dynamic withdrawals • cash reserve planning • Roth conversion opportunities during volatility Final ThoughtsThe bond market is changing. But higher yields are not automatically bad news. For years, investors complained: “Bonds yield nothing.” Now they do. The challenge is understanding: • which bonds you own • why you own them • and how they fit into a broader retirement strategy Because in today’s environment, simply “owning bonds” is not a strategy anymore. Managing them properly matters far more.

Mark Struthers, CFA, CFP®, CEPA, RMA® For current clients looking for a meeting:

This commentary is provided for general information purposes only, should not be construed as investment, tax, or legal advice, and does not constitute an attorney/client relationship. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable, but is not guaranteed. |

The Bond Market Has Changed. Retirement Planning Must Too

Categories

- 401k

- Backdoor Roth

- Bitcoin

- College Funding

- Crypto

- Economics

- Estate Planning

- Featured

- Feel Good

- Financial Planning

- Healthcare

- healthcare

- HSA

- Inflation

- Insurance

- Investing

- IRA

- Mega Backdoor Roth

- Open Enrollment

- Podcast

- Private Equity

- Retire Early

- Retirement

- Roth IRA

- SEPP

- Social Security

- Student Loans

- Taxes

- Traditional IRA

- Uncategorized

Share this post:

If you don’t have a plan and would like to get one, schedule a Discovery Meeting:

To health and wealth!

Mark Struthers, CFA, CFP®, CRC®, RMA®

For current clients looking for a meeting:

This commentary is provided for general information purposes only, should not be construed as investment, tax, or legal advice, and does not constitute an attorney/client relationship. Past performance of any market results is no assurance of future performance. The information contained herein has been obtained from sources deemed reliable, but is not guaranteed.